News & Media

Market Perspectives – First Quarter, 2026

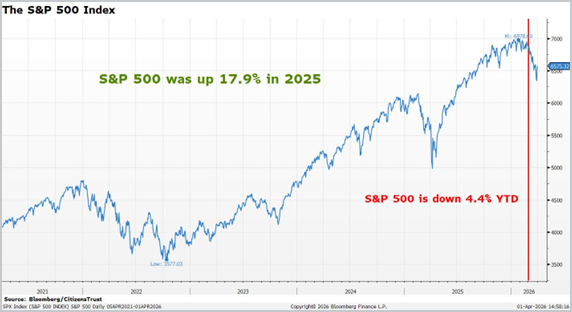

After a strong 2025, financial markets declined in the first quarter after the war in Iran created an oil supply shock that sent energy prices higher around the globe. The Federal Reserve remains on hold, and the market no longer expects any further rate cuts this year.

Equity Markets

The S&P 500 fell 4.4% in the first quarter. The broader market continued to climb in January and February and then pulled back as the conflict with Iran escalated. Wars tend to drive significant sector rotation, and this time was no different. The energy sector responded to higher oil prices and higher growth sectors like technology reacted negatively to potentially higher interest rates.

Many of the largest technology companies reported excellent earnings results coupled with large increases in their capital spending plans on AI. The upfront investment in AI infrastructure is massive and has investors concerned with the long-term returns as several companies are now spending most of their free cash flow on AI. All of the mega-cap tech stocks were down in the first quarter, contributing to the decline in the NASDAQ composite which fell 7.0%.

In the first quarter, mid-cap stocks, as measured by the Russell Mid-Cap ETF, gained 1.3% and small-cap stocks, as measured by the Russell 2000 Small-Cap ETF, gained 0.9%. Those ETFs were strong in the beginning of the quarter reaching new all-time highs but sold off in March after the war with Iran started. This pattern held for most global indices.

International equities also started off the year strong, only to sell off in March. Europe and Asia are big importers of oil and gas. Many international markets sold off more than the U.S. in March but still finished up for the quarter. International Developed markets, as measured by the EFA ETF, gained 1.2% during the quarter. Emerging markets, as measured by the EEM ETF, rose 3.8% in the quarter. Globally, the MSCI World Index declined 2.2% during the quarter due to weakness in large-cap U.S. tech stocks.

Interest Rates

The Federal Reserve made no changes to monetary policy during the first quarter, holding the federal funds rate steady at 3.75%. Fed Chair Jerome Powell projected this pause in interest rate policy and said it reflected an assessment of solid economic growth combined with inflation levels that remained somewhat elevated. Powell’s term as Fed Chair ends in May and President Trump has nominated Kevin Warsh to succeed him pending senate confirmation. The current Administration has argued quite publicly in favor of lower interest rates to boost economic growth.

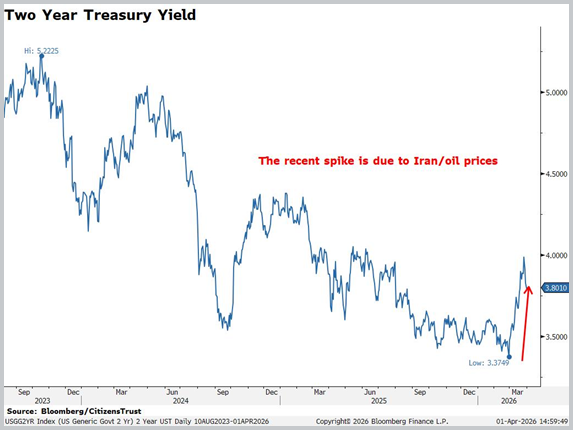

In January the market had expected further rate cuts in the back half of 2026, but the conflict in Iran has since eliminated any expectation of a lower fed funds rate this year. The 2-year Treasury yield promptly increased over 40 basis points once the hostilities with Iran were initiated. The inflationary effects of a sharp increase in global energy prices will undoubtably give the data-dependent Fed a lot to digest in the coming months. Longer-term markets rates were relatively steady, with the 10-year Treasury yield finishing the quarter modestly higher near 4.35%.

The Bloomberg Aggregate Index, a broad measure of the U.S. bond market, was essentially flat with a 0.05% decline for the quarter. While yields did rise after the beginning of the Iran conflict, the 10-year Treasury yield has been between 4.0% and 4.5% for most of the past two years.

The Economy

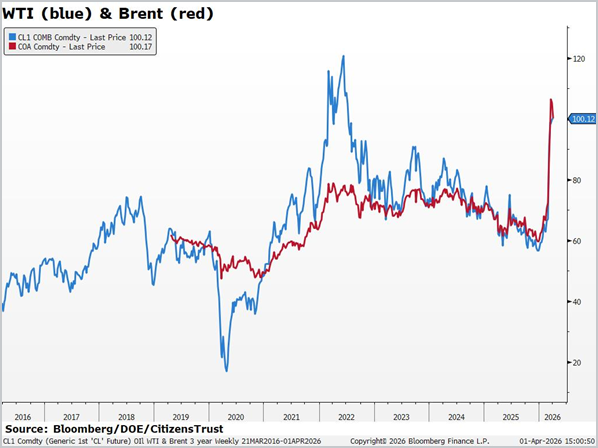

Economic indicators point to a strong U.S. economy in the first quarter. The large “services” portion of the economy continues to expand, and the more cyclical manufacturing sector has accelerated in recent months. The ISM Manufacturing survey jumped to 52.6 in January and has been above 50 (indicating expansion) for three consecutive months. This reflects the strongest manufacturing expansion since the summer of 2022, and the recent surge in wartime spending will likely add to manufacturing strength. Consumer spending has remained strong and in 2026 many consumers will benefit from the changes provided by the tax bill passed last year. Our domestic economic strength will be an important offset to the oil supply shock caused by the war with Iran. Oil prices have surged more than $40 per barrel and that burden will be felt throughout the second quarter and likely into the summer. Gasoline, diesel and jet fuel prices have spiked sharply, leading to a rise in inflation expectations for the rest of the year.

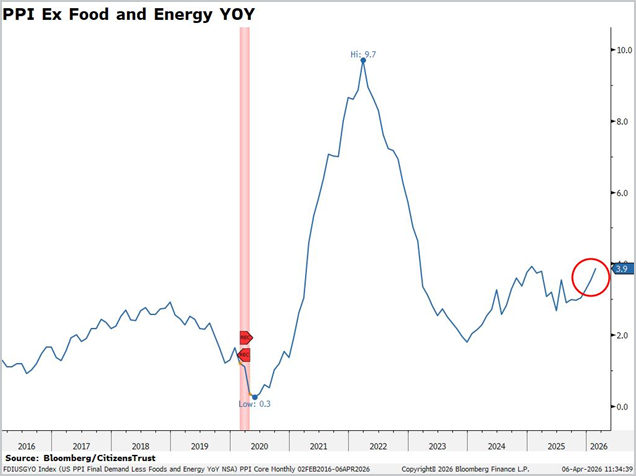

Most inflation indicators produce a “Core” measurement that excludes volatile inputs like food and energy. However, if higher energy prices persist, producers will eventually pass through their increased cost burden and increase prices of goods to the end consumer. Considering this, inflation “expectations” measured by the New York Fed have jumped into the mid three percent range. The upward pressure on inflation should first be seen in the Producer Price Index, which was already picking up in the first quarter.

The future Federal Reserve Chairman will be challenged to justify further rate cuts in the face of rising inflation, if it evolves. In 2025, the economy was surprised by tariff announcements, which increased inflation fears and impacted Fed policy. Today the economy confronts an energy shock, which is increasing inflation fears, and it will likely influence Fed policy for the rest of the year.

The Quarter Ahead

Investors will be acutely focused on oil prices and how long they remain elevated. Significant increases in energy prices that persist for several quarters have historically slowed economic growth. Thus, the duration of the conflict with Iran and how quickly it de-escalates will be the primary driver of all economic forecasts for the foreseeable future. While current “spot” prices of oil grab the headlines with violent price moves, forward oil contracts have not priced in an extended conflict with Iran. The December WTI oil contract is currently in the low seventy-dollar range, indicating the oil market does not expect the current high prices to endure for long.

Corporate earnings continue to grow at an impressive rate. Fourth quarter 2025 earnings as reported early in the year were strong – up 14% year-over-year. Earnings for the first quarter of this year, and the rest of 2026, are expected to grow at a similar pace. U.S. domestic investment is expected to remain a key driver of economic expansion in 2026. Capital spending on artificial intelligence infrastructure and data centers has expectations for business fixed investment (non-residential) to grow between 4% to 6% this year, providing a large source of support for the U.S. economy and spending that is largely indifferent to oil prices.

We look forward to serving you and appreciate the trust you have placed in us. Please reach out to your CitizensTrust representative with any questions you may have.

Learn more about CitizensTrust.

Content provided by: R. Daniel Banis, Executive Vice President, Head of CitizensTrust, and Donald Evenson, Senior Vice President, Chief Investment Officer.

CitizensTrust is a division of Citizens Business Bank, N.A.

Trust and Wealth Management are provided by CitizensTrust Wealth Management. The information provided is an opinion on economic outlook and not investment advice. The information is not offered with a product or service. This information is not intended to be a substitute for specific tax, legal, or investment planning advice. We suggest that you discuss your specific questions with your qualified tax, legal or investment advisor.

| Not Insured By FDIC or Any Other Government Agency ● Not Bank Guaranteed ● Not Bank Deposits Or Obligations ● May Lose Value |