News & Media

Market Perspectives – Second Quarter, 2026

Equity markets bounced back strongly in the second quarter while bonds struggled with the prospect of potential rate hikes. Higher inflation measures changed the expected path of interest rates but with the Iranian conflict on pause, oil prices reversed course and are back to where they were earlier in the year

Equity Markets

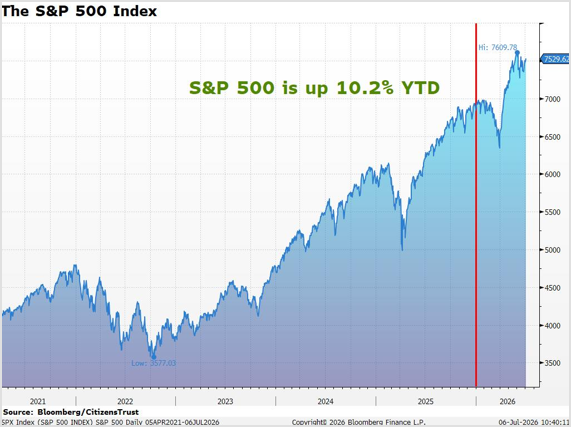

The S&P 500 rose 15.2% in the second quarter and is now up 10.2% YTD. The de-escalation of the war with Iran sent energy prices lower and AI related investment spending showed no signs of slowing. The technology sector performed the best in the second quarter while the energy sector fell alongside lower oil prices.

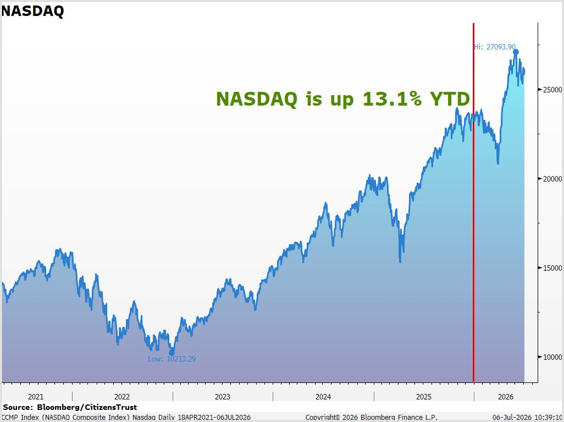

After its decline in the first quarter, the NASDAQ composite staged a bigger comeback than the S&P 500 in the second quarter, gaining 21.6%, which puts the YTD increase at 13.1%. The technology sector led the market in the number of companies issuing positive EPS guidance. In fact, it was the highest number of tech companies raising guidance since FactSet began tracking

In the second quarter, mid-cap stocks, as measured by the Russell Mid-Cap ETF, gained 13.8% and are now up 15.2% YTD. Small-cap stocks, as measured by the Russell 2000 Small-Cap ETF, rose a whopping 21.4% in the quarter and are now up 22.6% YTD. The strength in equities across market caps is a sign that individual stock participation has broadened beyond the mega-cap names that had dominated performance in previous years.

International equities also had a strong quarter as energy prices fell. Europe and Asia benefit the most from lower energy prices as they are big importers of oil and gas. Other International markets have benefitted from the high demand for semiconductor and memory chips. The Korean stock market which is dominated by large memory makers such as Samsung and SK Hynix is up 98% YTD. International Developed markets, as measured by the EFA ETF, gained 8.6% during the quarter and are up 9.9% YTD. Emerging markets, as measured by the EEM ETF, rose 21.1% in the quarter leaving the YTD gain at 25.7%. Globally, the MSCI World Index rose 14.2% during the quarter and is up 11.7% YTD.

Interest Rates

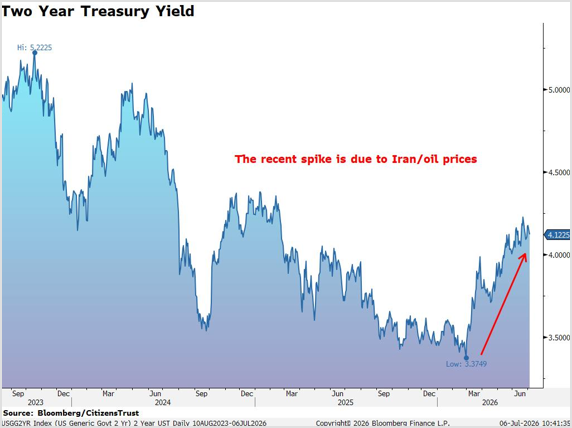

The new Chairman of the Federal Reserve, Kevin Warsh, had his first FOMC meeting in June and continued to hold the Fed Funds rate at its current level of 3.75%. While no changes to monetary policy have been made this year, the “easing bias” in their statement was removed. The Fed’s updated projections showed a more “hawkish” outlook, and several members anticipate one hike later this year. As usual, the two-year UST is ahead of the curve and with a current yield of 4.1%, it remains above the Fed Funds rate.

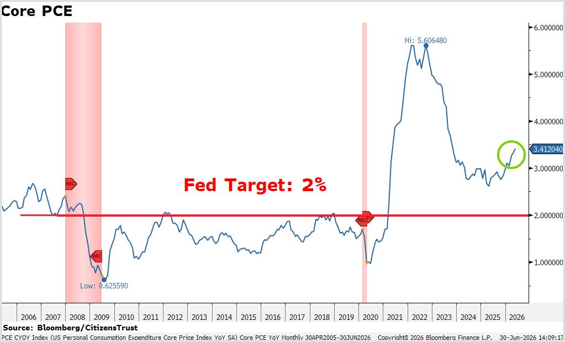

The expected upward bias to inflation, caused by the spike in energy prices has been the primary driver of higher two-year Treasury yields. However, it’s not just energy prices that have increased inflation. Home prices and rents have made gains on a national level even though home sales are very slow. Electronics and computer equipment have also seen rising prices as the AI capex boom has absorbed a lot of component capacity. Core PCE has been rising for a year now and is well above the Fed’s stated target of 2%.

With a relatively steady labor market, the Fed’s priority will be to fight inflation. Fortunately, oil prices have come back down, and we believe the Fed will take some time to see if that translates to lower inflation readings in the coming months. Chairman Warsh has long criticized the Fed’s forward guidance as not helpful for policy and we expect less forward guidance in the future, which will make the two-year yield a more significant indicator of where consensus expects rates to go.

The Bloomberg Aggregate Index, a broad measure of the U.S. bond market, gained 0.7% for the quarter leaving the YTD gain at 0.6%. While yields did rise after the beginning of the Iran conflict, the 10-year Treasury yield has been between 4.0 and 4.5% for most of the past two years.

The Economy

The U.S. economy has shown resilience, despite a war and an energy shock. Second quarter GDP growth will likely be around the 2.1% experienced in the first quarter, supported by AI-related business investment and a surge in oil exports. The large “services” portion of the economy continues to expand. The ISM Services PMI averaged 54 for the second quarter, indicating solid economic growth. The more cyclical manufacturing sector continued its recent strength with the ISM Manufacturing PMI averaging over 53 for the quarter. Crude oil has fallen over 30% from its post-Iran peak and gasoline prices are falling nationwide, providing some relief to consumers.

Inflation measures responded quickly to the sharp rise in oil, and they never seem to come down as fast as they go up. Core measures of inflation, which exclude food and energy, will need to come down as well for future rate hike expectations to dissipate. High inflation will continue to be the biggest influence on Fed policy for the rest of the year.

The Quarter Ahead

It appears we now have answer as to how long oil prices will remain elevated, as crude oil is back down to pre-war levels and the December futures contract for oil is below the current spot price. Nevertheless, energy prices will likely remain volatile given the current conditions in the Strait of Hormuz and globally low inventory levels. Oil prices, inflation measures, and the mid-term elections will be watched closely by investors in the coming months but are not likely to derail U.S. economic growth nor the significant gains in corporate profitability we are witnessing in 2026.

After a remarkable first quarter earnings report, S&P 500 earnings expectations continue to grow at an impressive rate. Typically, earnings estimates decline over the course of the quarter by an average of about three percent. In the second quarter, estimates rose 3.4%, marking the largest increase in bottom-up EPS estimates during a quarter since Q2 2021. Earnings are now projected to grow by over 23% YOY and if that turns out to be the case, it will be the second consecutive quarter of EPS growth above 20%. The earnings growth is broad based as well. At the sector level, nine of the eleven S&P 500 sectors have experienced upwardly revised earnings estimates over the past several months. With earnings rising at this pace, the market’s forward P/E multiple has declined over the past year and is roughly half a point higher than its five-year average.

We look forward to serving you and appreciate the trust you have placed in us. Please reach out to your CitizensTrust representative with any questions you may have.

Learn more about CitizensTrust.

Content provided by: R. Daniel Banis, Executive Vice President, Head of CitizensTrust, and Donald Evenson, Senior Vice President, Chief Investment Officer.

CitizensTrust is a division of Citizens Business Bank, N.A.

Trust and Wealth Management are provided by CitizensTrust Wealth Management. The information provided is an opinion on economic outlook and not investment advice. The information is not offered with a product or service. This information is not intended to be a substitute for specific tax, legal, or investment planning advice. We suggest that you discuss your specific questions with your qualified tax, legal or investment advisor.

| Not Insured By FDIC or Any Other Government Agency ● Not Bank Guaranteed ● Not Bank Deposits Or Obligations ● May Lose Value |